{kind=link}

Between the headlines about war, tariffs, and the layoffs blamed on either pandemic-era over hiring or artificial intelligence — depending on whom you ask — small businesses across America are quietly closing and disappearing.

It is not a story that leads cable news. The closures happen quietly, one storefront at a time. The data, however, suggest the pace is about to accelerate dramatically — and not for one reason, but for several reasons stacking on top of each other at once.

The squeeze that does not announce itself

The pressures hitting small businesses right now are dangerous mostly in combination. Inflation-era costs haven’t come back down, but customers have grown more price-sensitive. Payroll keeps climbing. Tariffs ripple through every supply chain, even for businesses that import nothing. Software subscriptions auto-renew into thousands per month in fixed overhead. And rent keeps rising — 52 percent of small-business owners saw rent increases in the past six months, and 41 percent could not pay their July rent in full. None of these is fatal alone. Stack them, and otherwise healthy businesses begin to struggle.

Kentucky’s economy is flatter than the narrative suggests

The Kentucky Chamber of Commerce reports the commonwealth ended 2025 with 5,700 fewer jobs than a year earlier, with negative or flat job growth in 10 of 12 months. The University of Kentucky projects 2026 employment growth at just 0.2 percent. Workforce participation lags most states.

Energy prices have moved hard against small businesses. Kentucky gasoline is about 40 percent above last year; diesel — the price that sets the floor for shipping and delivery — is 60 percent higher. Consumer sentiment hit a new all-time low in April. Economists describe the resulting picture as a “K-shaped” economy: higher-income households keep spending, lower-income households pull back. For a small-town diner whose customers sit in the second half, the K-shape is a thinner Tuesday lunch crowd.

When federal pullback hits Main Street

The federal infrastructure that small Kentucky communities lean on is being thinned out. The Kentucky Center for Economic Policy tracks the cuts. Three Kentucky Job Corps centers — including Morganfield’s, the second-largest in the country — were ordered closed in mid-2025. The IRS workforce has been cut by more than 25,000 employees, slowing the Earned Income Tax Credit that delivered $967 million to 352,000 Kentucky filers in 2023. Social Security layoffs will affect more than a million Kentuckians. The Patrick Leahy Local Food for Schools program, which connected over 130 Kentucky farmers to school cafeterias, has been ended.

The federal worker who lost a job is somebody’s customer at the diner. The school district that lost its local-food contract was somebody’s wholesale account. The EITC refund that arrives later, smaller, or not at all is the March receipt the local tire shop or hair salon used to count on.

The coming silver wave underneath all of this

Stack every single thing we mentioned with normal business pressures on a structural problem that has been building for a decade, and the closure pace makes sense.

Roughly half of all U.S. small businesses are now owned by people 55 and older. Yup, you thought it was hard for the young to buy a house, try owning a business. The central finding of Project Equity, the nonprofit tracking what it calls the “Silver Tsunami,” the wave of retirements that will, over the next decade, force tens of thousands of small-business owners to sell, hand the business down, or shut the doors. In south-central Kentucky, the picture varies sharply by county. Allen County is the regional bright spot: just 35 percent of businesses there are owned by people 55 or older, well below the national average. Every other county around it sits at or above the national benchmark:

- Barren County: 61% of businesses are owned by people 55+

- Edmonson County: 60%

- Simpson County: 51%

- Butler County: 49%

- Logan County: 48%

- Warren County: 43%

Statewide, Project Equity counts 31,615 Kentucky businesses with owners 55 and older — businesses that employ 360,000 people, run $13 billion in payroll, and generate $70 billion in revenue. More than 60 percent of small-business owners have no formal succession plan in writing.

When the timelines collide

An owner who is 67, running a business through the inflation hangover, watching payroll climb, absorbing a third rental increase, paying 30 percent more for gas, and noticing that the federal worker down the street no longer comes in for breakfast, is no longer thinking about a five-year succession plan. That owner is thinking about whether to keep going through next quarter.

The retirement wave and the acute pressure stack reinforce each other. The squeeze pulls the retirement decision forward. The absence of a succession plan turns retirement into closure rather than sale. When these businesses close, they do not get bought by Walmart. They do not get bought by anybody. They close.

The exception worth noticing

The small businesses around here that look most ready to survive a generational handoff are, almost without exception, the immigrant-owned ones. The taquerias. The mercaditos and international market. The nail salons. The auto shops where the lift never stops and somebody is always answering the phone in two languages. The restaurants where Abuela is still in the kitchen, grandkids are running the floor, and the kid who took your order is doing a chemistry problem set between tables.

The reason is not mysterious. It is not cultural mystique. It is not a TED talk about resilience. It is that these are family businesses in the actual working sense of the term. The second generation is already on the schedule, has been on the schedule since they were fourteen, and knows where the spare key to the back door lives. Succession is not a five-year plan. Succession is Tuesday’s shift.

It is also not an accident that this is the part of the regional small-business base that looks healthiest. According to the University of Kentucky’s Center for Business and Economic Research, Kentucky’s recent population growth has been driven primarily by immigration and immigrant family consolidation, with in-state migration of Kentuckians contributing far less. The people who are actually coming, staying, and building are the people whose businesses are already structured to outlast their founders. Unfortunately, many of those same owners have had to start making succession plans on a faster timeline than the demographic data would suggest — not because the business is in trouble, but because federal immigration policy keeps moving the ground underneath them.

Now look at the legacy small businesses. The ones built in the seventies and eighties and nineties. The owner is sixty-eight. The owner runs it. The owner has run it for forty years. The kids went to UK or Vandy, or moved to Nashville, Louisville (why?), or Atlanta. The kids are in real estate, healthcare administration, or finance. The kids are very nice and call on Sunday. The kids are not coming back to run the muffler shop.

The contrast is not a judgment of either group. But if we are going to have an honest conversation about who is actually going to be standing behind a counter in our region in 2036, we should probably start by looking at the people already doing it on a Tuesday afternoon.

How do we stop it?

A few responses, none of them magic:

BUSINESS OWNERS. Start succession planning now. A clean handoff takes three to five years. Owners who wait until they “feel ready” wait too long.

Pull an honest look at the cash flow. Which costs are growing without scrutiny? Which subscriptions still earn their keep (trust me we audit these for businesses and some are ridiculous)? Is the lease renewal a place to renegotiate or is it worth even moving? A proactive review buys runway for a deliberate decision instead of a forced one.

Consider employee ownership. A central recommendation from some think tanks is a conversion through worker cooperatives or ESOPs, paying the owner out over time from the business’s existing cash flow. The financing piece has gotten harder, the federal Community Development Financial Institution Fund, which capitalized the lenders most likely to finance an employee buyout, was disbanded earlier this year. CDFIs themselves still operate. The path is narrower than a year ago, not closed.

Consider community ownership. A growing number of small towns have purchased their local groceries, pharmacies, and hardware stores through community ownership when no private buyer would step forward.

Customers have a role. Spend at the places you would be sad to lose. Ask the owners whether they have a plan.

You can talk 2050 but who cares if it’s gone by 2036

The reason small businesses are closing is not a single villain. It is the stack — inflation that won’t fully unwind, a lease that doesn’t flex, gas prices dictated by a war of choice, federal programs being pulled back, a customer base in the lower half of a K-shaped economy, and an owner generation aging out without a plan. Any one of those, a healthy business survives. All of them at once is something else.

Stopping it requires the same answer at every level: planning that starts now, owners willing to talk honestly about what comes next, employees and communities willing to step in as buyers, customers willing to spend at the places they would be sad to lose, and policy that does not make the financing piece harder than it already is.

The Silver Tsunami is not a forecast. The uncertain state of our federal government trickling down we can’t do much about. The way Frankfort is being run, forget about it, nobody will rescue us there. What we have is the current condition of small-town commerce across most of south-central Kentucky, happening underneath the headlines, on a timeline the headlines have not yet caught up to.

The decade ahead will determine how much of it survives.

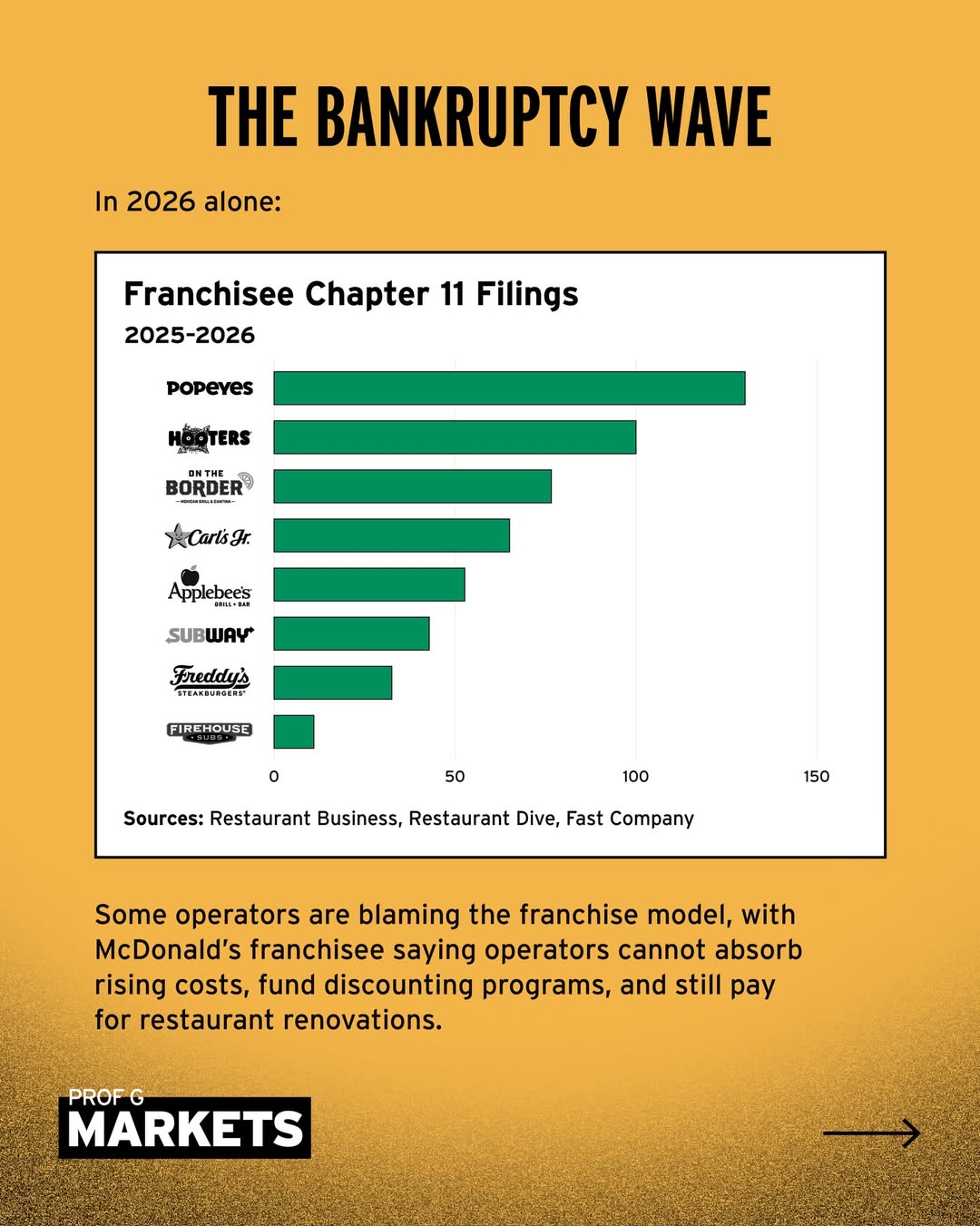

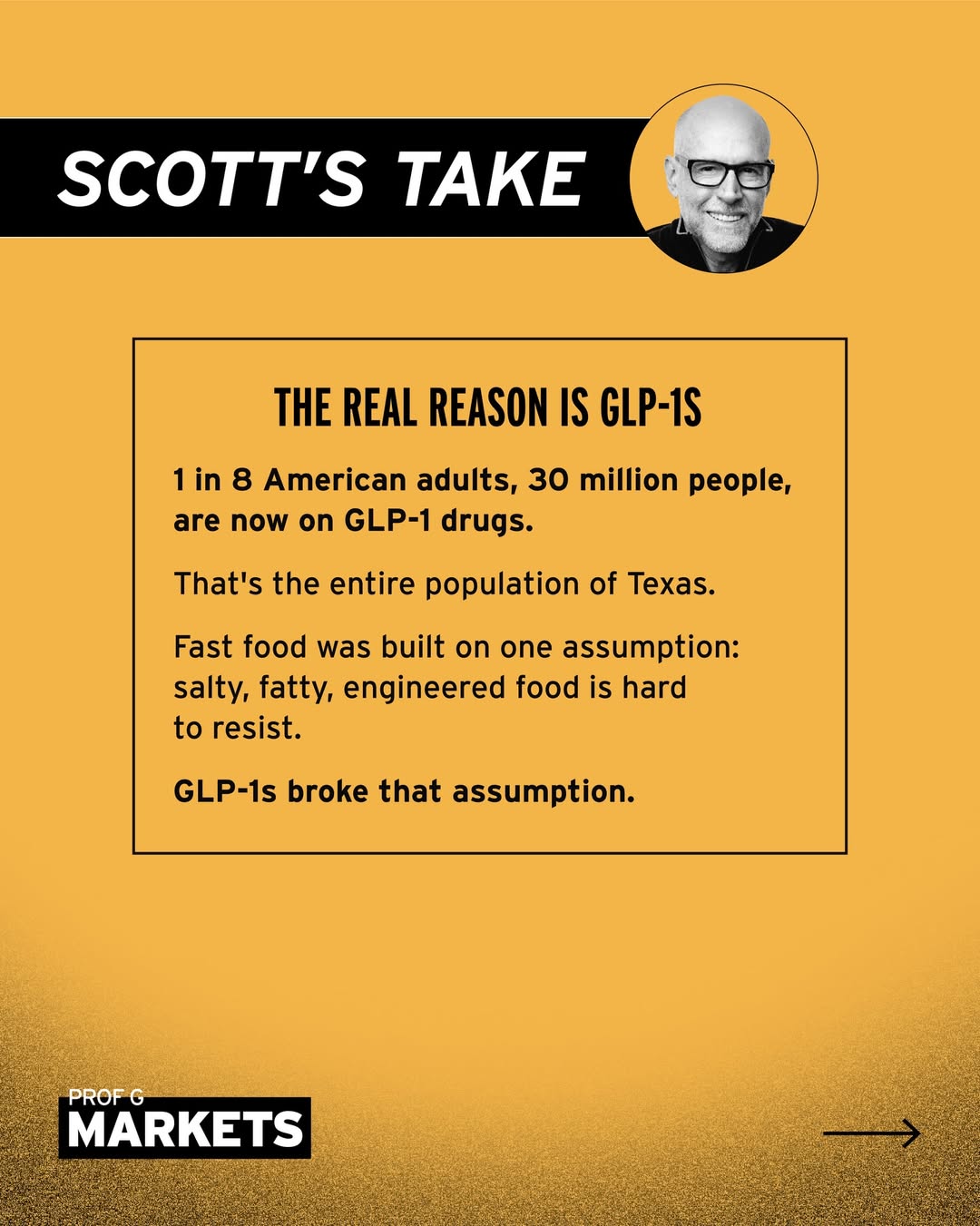

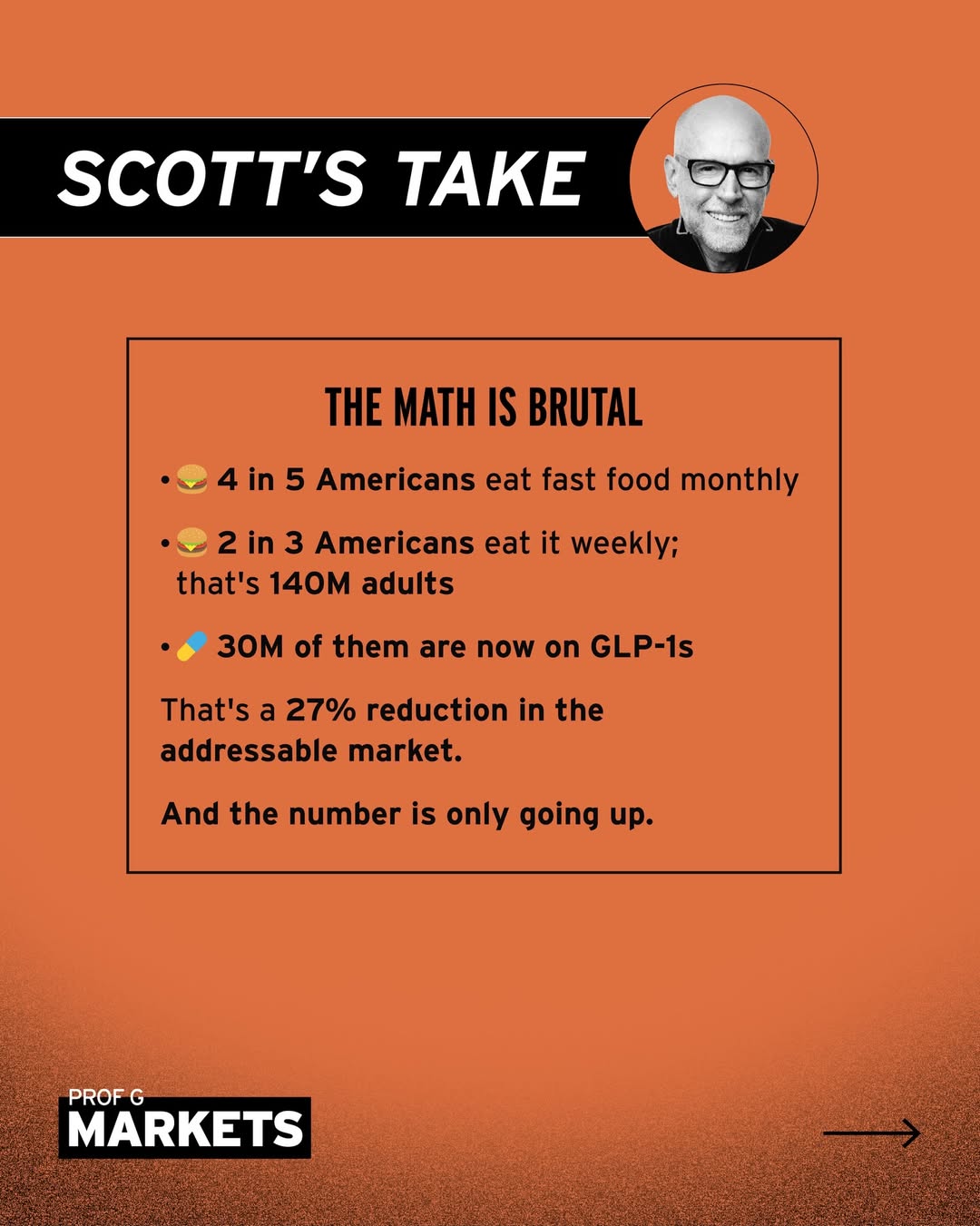

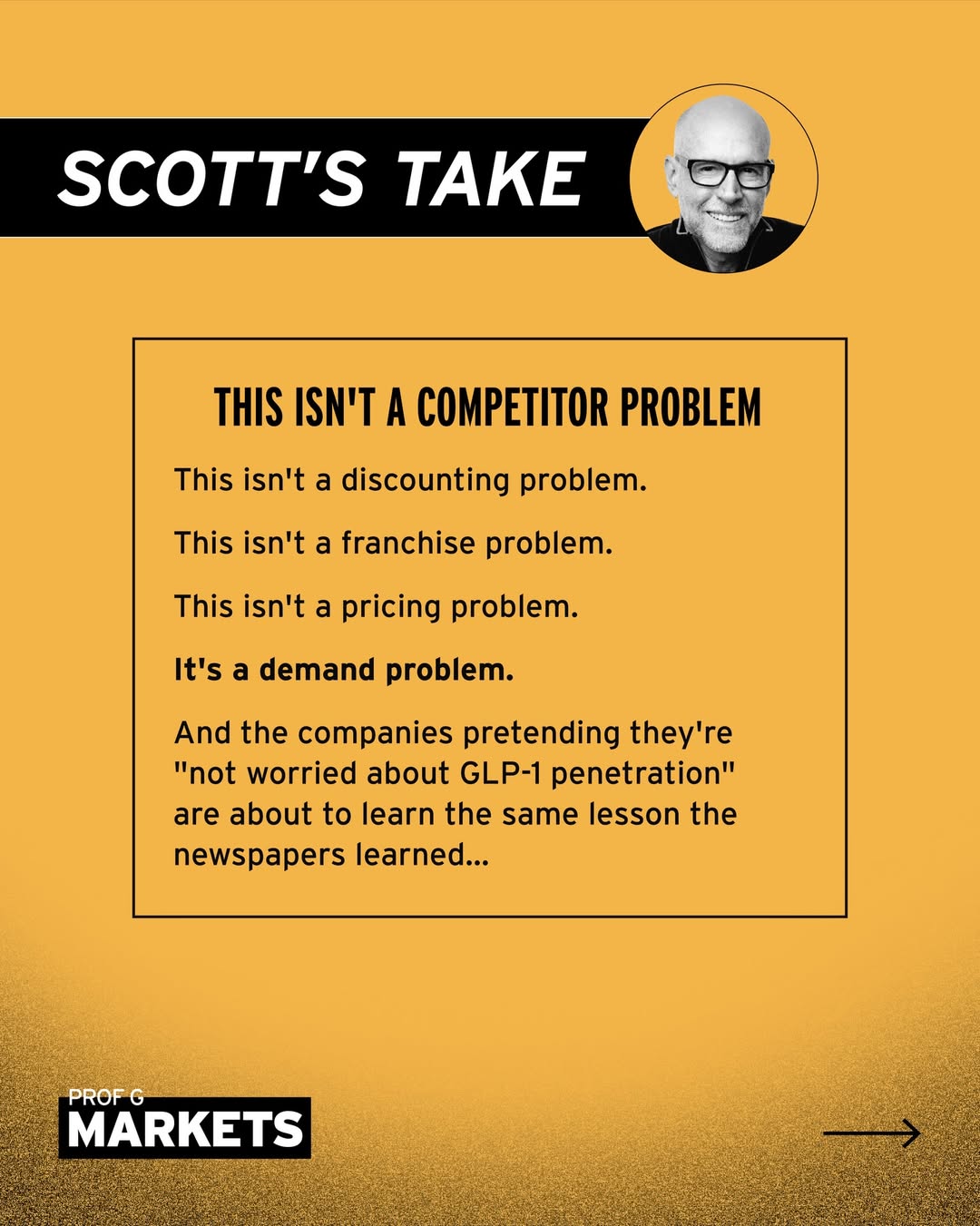

Before hitting “Publish” on this Blog apparently it’s not just local Businesses. This from Professor Scott Galloway: